Moving on from IR35 irritation, to action

Antecedentes

As regras de trabalho fora do pagamento-comumente conhecido como IR35-têm como objetivo garantir que indivíduos que trabalhem como funcionários pagem amplamente os mesmos impostos de emprego que os funcionários, independentemente da estrutura que trabalham. O IR35 se aplica quando um indivíduo (o 'trabalhador') fornece seus serviços através de um ou mais intermediários (geralmente empresas limitadas), a outra entidade (a 'End Engager'). Em abril de 2017, a legislação foi reformada para quem trabalha no setor público, com as autoridades públicas se tornando responsáveis por decidir se o trabalhador seria considerado um funcionário para fins de impostos sobre emprego se estivessem envolvidos diretamente. NICs sob Paye ao HMRC, em nome do trabalhador. Independentemente de o 'pagador de taxas' ser a própria autoridade pública, ou um agente.

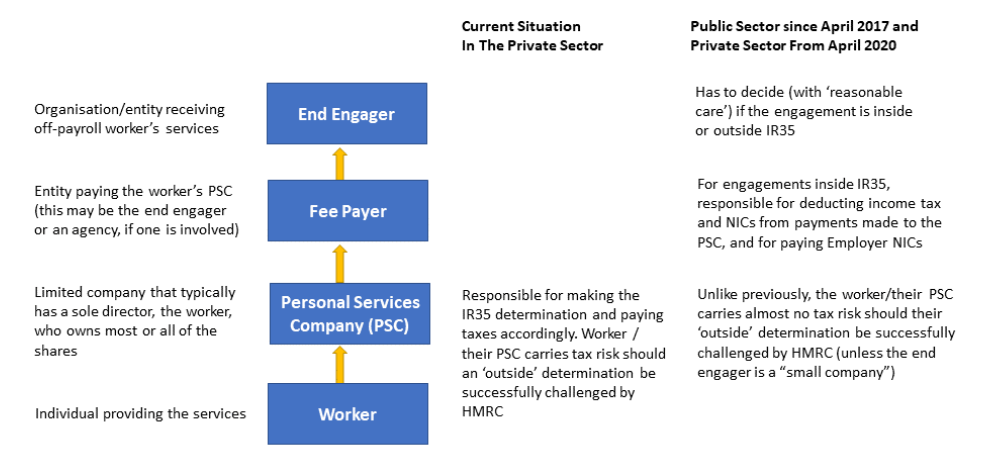

IR35 was introduced in 2000, with workers (limited company contractors, otherwise known as personal service companies – PSCs) being responsible for making their own IR35 determination and paying their taxes accordingly. In April 2017, the legislation was reformed for those working in the public sector, with the public authorities becoming responsible for deciding whether the worker would have been regarded as an employee for employment tax purposes if they were engaged directly.

In addition, if the worker was deemed to be working like an employee (‘inside IR35’), the entity which paid the worker’s PSC (the ‘Fee Payer’) became responsible for accounting for and paying income tax and NICs under PAYE to HMRC, on behalf of the worker. This was regardless of whether the ‘Fee Payer’ was the public authority itself, or an agent.

As widely anticipated, the following year it was announced that this reform would be extended to engagements in the private sector[1] from 6th April 2020. Estimates of the number of individuals affected range from 170,000 to 900.000 Empreiteiros de empresa limitada sediada no Reino Unido.

[1] A única exceção são empresas "pequenas", que não serão afetadas pela reforma. Como negócios independentes, eles carregam o risco financeiro associado a não ser cobrável aos clientes, permitindo que nossas taxas de taxas sejam inferiores às empresas tradicionais de consultoria baseadas em funcionários

em desacordo com o futuro do trabalho? Havia também um dreno de talento relatado, com os trabalhadores optando por procurar tarefas alternativas no setor privado, impactando negativamente a transformação no setor público. Parece uma direção de viagem em todos os ganhos; Para organizações que desejam explorar a força de trabalho "sob demanda" para permanecer ágil e flexível no meio das demandas de mercado [2] e para uma força de trabalho profissional que está cada vez mais optando por freelancer [3].

Issues with public sector reforms have been widely reported and included problems with the CEST (‘Check Employment Status for Tax’) determination tool and successful challenges to rulings. There was also a reported talent drain, with workers opting to seek alternative assignments in the private sector, negatively impacting transformation within the public sector.

In some ways it would seem a little incongruous that the government would seek to set obstacles in the path of the future of work. It seems a win-win direction of travel; for organisations that are keen to tap into ‘on demand’ workforces to stay agile and flexible in the midst of changing market demands [2] and for a professional workforce that is increasingly opting to freelance[3].

Talvez a economia profissional do show seja vítima de seu próprio sucesso? Com previsões que variam da modelagem mundial do Fórum Econômico, que a maioria da força de trabalho dos EUA será freelancer por 2027 e outras fontes dizendo 42% dos profissionais de RH planejam envolver trabalhadores mais contingentes no futuro, está claro para ver por que o HMRC pode ser assustado pelo impacto dessa tendência indiscutível nos cofres. De fato, acredita que menos de 10% dos PSCs realmente cumpriram suas responsabilidades e estima que o custo tributário possa chegar a £ 1,3 bilhão em 2023/24 [4]. A grande maioria dos consultores independentes, 86% está satisfeita em trabalhar como independente e está mais satisfeita do que os consultores empregados com sua vida profissional atual. [4] Trabalho fora do Payroll: Como as regras do IR35 afetam o setor privado | Orientação legal | Ferramentas | Xperthr.co.uk

[2] According to Mercer’s latest Global Talent Trends study, 79% of executives expect that contingent and freelance workers will substantially replace full-time employees in the coming years.[3] The vast majority of independent consultants, 86% are satisfied with working as an independent, and are more satisfied than employed consultants with their current professional life.[4] Off-payroll working: How IR35 rules affect the private sector | Legal guidance | Tools | XpertHR.co.uk

de irado à ação

Sua política claramente coerente para o governo querer identificar 'emprego blindado' e garantir que a tributação justa seja cobrada e concordamos com esse objetivo; but we also share the scepticism of many about the factors that HMRC believe make some engagements ‘employment -like’ given the financial risks independent consultants take on and wonder at the fairness of being deemed ‘employed’ for tax purposes but not for rights such as holiday and sick pay [5]

Whilst it is fair to say that there have been many shocks in our political landscape over the last year or so and there is lobby para revogar essa reforma controversa; Agora, é essencial em nossa opinião que todas as partes interessadas da 'cadeia de suprimentos'-consultores, clientes e empresas como nós mesmos procuram resolver as ambiguidades em andamento juntos e estamos bem em ação antes de abril. Em geral, nos envolvemos com nossos clientes por meio de:

As a consulting company we contract with our clients for the completion of project-specific activities and deliverables, i.e. contract for services, not for the provision of a specific person. In general, we engage with our clients through:

- Um contrato de serviços mestrado / estrutura para a prestação de serviços de consultoria, em conjunto com

- Uma declaração de trabalho para cada projeto. Projetos, esperamos que a maioria caia "fora" do IR35. No entanto, antecipamos que alguns dos nossos

Given the nature of the work and the degree of control we have over full service and managed capability consulting projects, we expect the majority to fall ‘outside’ of IR35. However, we do anticipate that some of our Consultoria intermediária As atribuições serão consideradas "dentro" do IR35 devido a políticas de clientes ou práticas de trabalho e, nessas instâncias, isso se comunicará com os que se comunicarão, que os consultores provavelmente serão solicitados a uma empresa que se comunicará recentemente, que se comunicará com a empresa que se comunicará com a empresa que se comunicará com a empresa que se comunicará, que se comunicará com os que se comunicam, que se comunicarão, que se comunicarão, que os consultores são os que se reúnem, que os consultores provavelmente serão solicitados a uma empresa que se comunicará, que se comunicará, que se comunicará, que se refere a que os consultores e os consultores provavelmente serão solicitados a uma empresa que se comunicará com isso. Devido ao lançamento em dezembro de 2019, mas sob orientação atual, para uma oportunidade de ser considerada 'fora do IR35', existem três condições principais, qualquer um dos quais consideraria um engajamento como 'fora' do IR35:

We welcome the recent HMRC briefing which refers to planned improvements to the CEST tool, now due for release in December 2019, but under current guidance, for an opportunity to be considered ‘outside IR35’, there are 3 main conditions, any of which would deem an engagement to be ‘outside’ of IR35:

- deve haver um à direita da substituição || 114 . The consultant can provide a substitute if he/she is unable or unwilling to do the work and the client has no right of veto as long as substitute has the right skills/qualifications. The original consultant must bear the costs of this substitution.

- The client does not supervise, direct or control how the consultant delivers the services . Our consultants will work to the scope, objectives and deliverables agreed between B2E Consulting and the end client, but they will use their own expertise to decide how the work is performed and to some extent, where the work is performed e.g. split between home office and client site working.

- There is no mutuality of obligation. There is no obligation, at the end of the current contract, for the client to offer more work to B2E/the consultant and if more work were offered, there is no obligation for B2E/the consultant to accept such work. Similarly, during the existing contract, there is no obligation for the consultant to provide any services outside of those documented on the Statement of Work; if the client requires different/additional services, these need to be the subject of a change request to the existing contract,

Existem outras considerações, incluindo:

- Parcel e Parcela: Os consultores não devem ser tratados como funcionários e não devem receber os mesmos benefícios que, por exemplo

- Risco Financeiro: Os consultores devem demonstrar algum risco financeiro em torno da prestação dos serviços - por exemplo, Se o retrabalho for necessário, deve ser feito com o próprio custo e despesa do consultor. Embora seja aceito que, na prática real, o cliente pode fornecer um PC do ponto de vista de segurança de TI,

- Exclusive Service: Nothing in the contracts should prevent the consultant from performing paid work for more than one client concurrently (related to ‘control’).

- Provision of Equipment: Consultant should provide their own business equipment to enable them to deliver the services for which they have been engaged. Although it is accepted that in actual practice, the client may provide a PC from an IT security point of view,

- sendo em negócios na conta do consultor - sendo registrado no IVA; Tendo seus próprios seguros Pi e PL, tendo endereço de e-mail de trabalho etc.

[5] https://www.qdoscontractor.com/docs/default-source/Resources/Contetrocutorh. IR35, dependendo do perfil de risco e das práticas de trabalho. Estamos trabalhando com eles e especialistas como

Outlook

Ultimately each client will have a different approach that they will wish to take to IR35 depending on their risk profile and working practices. We are working with them and experts like QDOS para ajudar a trazer nossos clientes e nossos consultores mais clareza nos próximos meses. Prevemos que a tendência para acordos de trabalho mais flexíveis continuarão apesar das mudanças no IR35; Os clientes ainda desejam manter uma mistura de talento em seus negócios e, portanto, a demanda por opções flexíveis de talentos permanecerá. Intensifica

We foresee a large increase in the use of umbrella companies as a way to respond to this new legislation whilst complying with the new IR35 obligations. We anticipate that the trend towards more flexible working arrangements will continue despite the changes to IR35; clients will still want to maintain a mix of talent within their businesses and therefore demand for flexible talent options will remain.

Sources / Further Reading

Hunts Canlon – Human capital leaders turning to flexible workforce in record numbers

The HR Director – Gig economy booms as war for digital talent intensifies

Consultancy UK - Independentes mais satisfeitos com a carreira do que os consultores empregados

Global News Wire - Como ser uma estrela do rock no segmento de especialistas em elite da economia do gig

Personnel Today – Gig professionals on the rise and HR likes it

We Forum – 4 Predictions for the future of work

Business.com – Here’s how small businesses benefit from freelance talent

Contabilidade diária-HMRC esclarece as regras do IR35 para os trabalhadores fora do roll

Gov.uk-HMRC Edição Briefing: Reforma do Prayroll Ruias de Trabalho ROURS. Setor Aprenda da maneira mais difícil

Consultation document: Off-payroll working rules from April 2020.pdf

XpertHR – IR35 – Will the private sector learn the hard way

It Contracting.com-IR35

Computing.co.uk-Governo para avançar com as reformas do IR34

Empreiteiro semanal-Rbs para interromper os contratantes do IR35 Ur35 | Empreiteiro - Guia do Empreiteiro para Reforma IR35

Consultancy UK – HMRC’s IR35 change: an opportunity for consulting firms?

Qdos Contractor – Contractor Guide to IR35 Reform

ODGERS INTEM - IR35 E O SETOR PRIVIDO

Procrere - Spotlight on Ir35 Relatório

Sobre o autor, Maninder Murfin || 178

Maninder joined B2E in 2015 and works with our clients and consultants as a Service Delivery Partner. She also leads the Business Analysis capability talent pool and B2E’s social media activities. Prior to this, Maninder spent nine years with Accenture within its UK Financial Services division, leading and supporting programme workstreams in Change Management, TOM Design, Organisation Design and HR Transformation.

About the author, Maninder Murfin

Maninder joined B2E in 2015 and works with our clients and consultants as a Service Delivery Partner. She also leads the Business Analysis capability talent pool and B2E’s social media activities. Prior to this, Maninder spent nine years with Accenture within its UK Financial Services division, leading and supporting programme workstreams in Change Management, TOM Design, Organisation Design and HR Transformation.